Purchasing a home is one of the most significant financial decisions in any Indian household. With the Reserve Bank of India (RBI) maintaining a calibrated monetary stance in 2026, home loan interest rates remain relatively attractive, making this an opportune time for homebuyers to explore their financing options.

Best home loans in India for 2026 feature competitive interest rates starting from around 7.10%–7.50% p.a., with major lenders offering tenures of up to 30 years. Key lenders include SBI, HDFC, ICICI, Bank of Baroda, PNB, LIC Housing Finance, and Axis Bank, targeting low EMIs and financing up to 90% of property value.

Key Considerations Before Choosing a Home Loan

Before diving into the best home loan options, it is essential to understand the core parameters that determine the suitability and affordability of a home loan:

Interest Rates: As of early 2026, the lowest home loan rates are around 7.10%–7.50% p.a. Rates are either fixed or floating (linked to RLLR/MCLR/Repo Rate). Floating rates are generally lower and reset periodically.

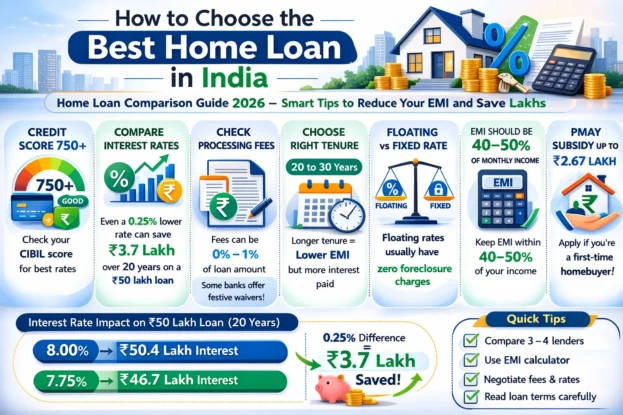

Eligibility: A credit (CIBIL) score of 750 or above significantly improves the likelihood of securing the lowest interest rate. Income stability, employment type, age, and existing liabilities also play a crucial role.

Processing Fees: Range from NIL to 1% of the loan amount. LIC Housing Finance offers one of the lowest fees, starting at 0.25%, while some private lenders may charge up to 1%–2%.

Tenure: Repayment tenures of up to 30 years are widely available, substantially reducing monthly EMI burdens. A longer tenure means more total interest paid, so borrowers should balance EMI comfort with overall cost.

Foreclosure Charges: RBI mandates zero foreclosure charges for floating rate home loans for individual borrowers. Fixed-rate loans may attract charges of 2%–4% of the outstanding principal.

Loan-to-Value (LTV) Ratio: Most lenders finance up to 75%–90% of the property value, depending on the loan amount and borrower profile.

PMAY (Pradhan Mantri Awas Yojana): First-time homebuyers in EWS/LIG/MIG categories may be eligible for interest subsidies under the PMAY-Urban scheme.

Quick Comparison: 14 Best Home Loans at a Glance

Lender

Interest Rate (p.a.)

Processing Fee

Max Tenure

1. SBI (State Bank of India)

From 7.25% p.a. (floating, linked to RLLR)

0.35% of loan amount

Up to 30 years

2. LIC Housing Finance

From 7.15% p.a. (one of the lowest in the market)

0.25% of the loan amount + GST

Up to 30 years

3. ICICI Bank

From 7.45% p.a. (floating; linked to RLLR)

Up to 0.50% of the loan amount + GST

Up to 30 years

4. Bank of Baroda

From 7.20% p.a. (linked to RLLR)

0.25%–0.50% of the loan amount

Up to 30 years

5. HDFC Bank

From 7.75%–7.90% p.a. (floating rate)

Up to 0.50% of the loan amount or ₹3,000

Up to 30 years

6. Punjab National Bank (PNB)

From 7.20% p.a. (linked to RLLR)

0.35% of loan amount

Up to 30 years

7. IDBI Bank

From 7.35% p.a. (floating rate, RLLR-linked)

0.50% of the loan amount + GST

Up to 30 years

8. Axis Bank

From 8.00%–8.35% p.a. (floating rate)

Up to 1% of the loan amount + GST

Up to 30 years

9. IDFC FIRST Bank

From 8.85% p.a. (floating rate)

Up to 0.50% of the loan amount + GST

Up to 30 years

10. Bajaj Housing Finance Limited

From 8.60% p.a. (floating rate)

Up to 0.35% of loan amount + GST

Up to 32 years (one of the longest tenures available)

11. Union Bank of India

Around 8.70% p.a. (floating rate, RLLR-linked)

0.50% of loan amount

Up to 30 years

12. Kotak Mahindra Bank

From 7.70% p.a. (floating rate)

Up to 0.50% of loan amount + GST

Up to 20 years

13. Federal Bank

From 8.75% p.a. (floating rate)

0.50% of loan amount + GST

Up to 30 years

14. India Shelter Home Loan

Around 8.43%–16% p.a. (varies by profile)

1%–2% of loan amount + GST

Up to 20 years

Detailed Review of 14 Best Home Loans in India

1. SBI (State Bank of India)

Interest Rate

From 7.25% p.a. (floating, linked to RLLR)

Eligibility

Credit score 750+; salaried/self-employed individuals; minimum income as per bank norms

Processing Fee

0.35% of loan amount (min ₹2,000, max ₹10,000) + GST

Tenure

Up to 30 years

Foreclosure Charges

NIL for floating rate loans; applicable for fixed rate

Highlights

India’s largest lender; transparent fee structure; wide branch network; SBI Privilege & Shaurya schemes for govt. employees & defence personnel

Strong NRI-focused home loan products; Pravasi Home Loan for diaspora; joint loan option; good customer service in Kerala and South India

14. India Shelter Home Loan

Interest Rate

Around 8.43%–16% p.a. (varies by profile)

Eligibility

Credit score 600+; caters to first-time buyers & low-income segments; informal income accepted

Processing Fee

1%–2% of loan amount + GST

Tenure

Up to 20 years

Foreclosure Charges

2%–4% on outstanding principal (applicable charges)

Highlights

Focused on affordable housing and Tier 2/3 cities; accepts informal income proof; PMAY-linked subsidies available; ideal for underserved borrowers

How to Choose the Right Home Loan

Selecting the ideal home loan depends on several personal and financial factors:

Compare Interest Rates: Use online EMI calculators to compare total repayment amounts across lenders. Even a 0.25% difference can save lakhs over a 20–30 year tenure.

Check Your Credit Score: Obtain your CIBIL score before applying. A score of 750+ ensures access to the best rates. Address any discrepancies in your credit report beforehand.

Evaluate Processing Fees & Hidden Charges: Look beyond the interest rate — processing fees, legal charges, technical evaluation fees, and prepayment penalties add to your total cost.

Assess Loan Tenure: Longer tenures reduce EMI but increase total interest. Use a tenure that keeps EMI within 40%–50% of your net monthly income.

Opt for Floating Rate: In a declining rate environment, floating rates (linked to RLLR/Repo Rate) benefit borrowers with reduced rates when RBI cuts the repo rate.

Consider Balance Transfer: If you have an existing high-interest home loan, consider transferring to a lender offering lower rates. Factor in processing and legal fees before switching.

PMAY Benefits: First-time homebuyers should check eligibility for Pradhan Mantri Awas Yojana (PMAY) interest subsidies of up to ₹2.67 lakhs.

Pro Tips for Home Loan Applicants in 2026

Maintain a CIBIL score of 750 or above for the best rates — pay all EMIs and credit card dues on time.

Apply jointly with a co-applicant (spouse, parent) to increase loan eligibility and sometimes avail lower rates.

Women borrowers receive preferential interest rates (0.05%–0.10% concession) at many PSU banks, including SBI and Bank of Baroda.

Avoid multiple simultaneous loan applications — each hard inquiry reduces your CIBIL score by a few points.

Negotiate processing fees — many lenders waive or reduce them for high-value borrowers or during festive seasons.

Keep documents ready: KYC, income proof (ITR/salary slips), bank statements, property documents, and employer certificate.

Review the loan agreement carefully — pay attention to rate reset clauses, prepayment conditions, and insurance bundling.

Conclusion

The Indian home loan market in 2026 is highly competitive, with both public sector banks and private lenders offering attractive rates, flexible tenures, and borrower-friendly features. SBI, LIC Housing Finance, and Bank of Baroda stand out for their low interest rates and minimal fees, making them ideal for cost-conscious borrowers. ICICI Bank, HDFC Bank, and Kotak Mahindra Bank offer superior digital experiences and quick processing.

For affordable housing seekers, India Shelter Home Loan and Union Bank of India cater to Tier 2/3 cities and lower-income segments. Self-employed individuals may find IDFC FIRST Bank and Bajaj Housing Finance more accommodating with their flexible income assessment criteria.

Ultimately, the best home loan is one that offers a combination of a low interest rate, minimal fees, flexible repayment, and a lender with a strong service track record. Use the information in this guide as a starting point — always verify the latest rates directly with lenders or through aggregator platforms like Paisabazaar or BankBazaar before finalizing your decision.

Interest rates, fees, and other loan terms mentioned in this document are indicative as of early 2026 and are subject to change at the discretion of the respective lenders. Please verify all rates and charges directly with the lender or their official website before making any financial decisions. This content is for informational purposes only and does not constitute financial advice.

With over 2000 articles and blogs to his name for Flickonclick, Mohan Nasre is a versatile content writer skilled in multiple niches, including entertainment, technology, finance, news, lifestyle, fitness, and more. His dynamic writing style and ability to adapt to diverse topics have made him a go-to writer for high-quality, engaging content that resonates with readers across various industries.