When I first heard you could use credit card for upi payments, I figured it was one of those features that technically exists but is too annoying to actually use.

Fast forward to last month.

I’m sitting in a Bangalore cafe that makes incredible filter coffee for ₹35. Already ordered, already sitting down. Then I check my bank balance. ₹247 staring back at me. My order was ₹420. Credit card was at home, and canceling after anticipating that coffee for 47 minutes felt unbearable.

That’s when I remembered this UPI-credit card thing was actually real.

So I Set It Up Right There

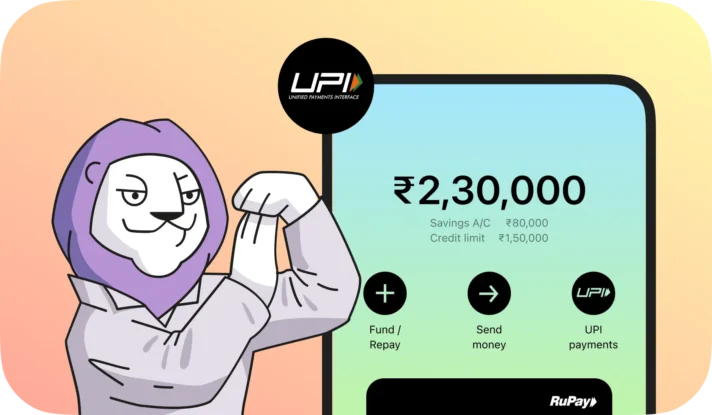

Opened PhonePe could’ve used Google Pay or Paytm, but PhonePe was already open. Found payment methods, tapped “Add Credit Card,” typed my RuPay credit card details 16 digits, expiry, CVV. OTP came through. Set up a UPI PIN for the card.

Done. 3 minutes tops.

I scanned the cafe’s QR code, picked my newly added credit card instead of my bank account, entered my PIN, and paid. The guy at the counter had zero clue I’d used a credit card because it looked identical to every other UPI payment.

Why I Think More People Should Know About This

I’ve used UPI since 2018, but back then you could only link bank accounts. You needed actual money in savings. If your balance was low, tough luck.

Banks started letting RuPay credit cards link with UPI around 2022, but it flew under the radar. I’ve found this genuinely useful in unexpected ways.

Also Read: Best Stocks to Buy This Month

Like when salary hasn’t hit yet but bills are due that painful stretch between the 25th and 1st where you’re avoiding your balance. If you need groceries or fuel and your account is empty, you tap into your credit limit instead.

Or when friends send a UPI request for ₹1,240 because they covered dinner, but you won’t have money until payday. Instead of sending an awkward “can you wait till Friday” message, you pay immediately using your credit card through UPI.

I used this during an online sale. Phone was ₹24,999. I had money, just not quite enough. Instead of transferring funds or missing the sale, I paid via UPI using my credit card. Got the deal, zero hassle.

But Here’s What You Should Actually Know

Not perfect though. Some people might shoot themselves in the foot.

First, you can’t send money directly to friends yet. You can only pay merchants shops, websites, restaurants, anyone with a business QR code. Person-to-person transfers still require your bank account.

Second, transaction limits vary. Mine was ₹50,000 per transaction, but some banks cap at ₹25,000 or bump to ₹1,00,000. Check yours.

Third—you’re still using a credit card. Borrowed money. If you don’t pay your bill when due, interest piles up. Not free money just because it comes through UPI.

Also, only RuPay credit cards work. Got Visa or Mastercard? Out of luck. Banks are working on expanding this, but right now RuPay is your only option.

What I’ve Been Doing Differently

I used to carry my physical credit card everywhere. Now I don’t bother. My wallet is noticeably lighter. I pay for most stuff via UPI anyway, so having my card linked makes more sense.

But I started tracking spending way more carefully. When you swipe a physical card there’s a process hand it over, wait, enter PIN, get it back. Your brain registers “I just spent money.”

With UPI everything happens in 4 seconds. Scan code, select payment, enter PIN, done. So fast you forget you’re spending real money. When that spending is on a credit card where you’re not seeing your balance drop? Even easier to lose track.

Now I check my credit card statement every week instead of monthly. Set a Saturday reminder. Just scroll through transactions to know what I’ve been spending.

Are There Any Charges?

Most UPI apps don’t charge extra for linking a credit card. PhonePe didn’t charge me. Google Pay and Paytm were the same. The UPI transaction is free, like normal UPI payments.

But your credit card might have its own rules. Some banks charge fees for certain payment types “fuel surcharge” or “convenience fee.” I haven’t been charged extra yet, though I’ve mostly used this for groceries and purchases under ₹2,000.

For big purchases like rent or laptops, check your credit card terms first. Some banks treat UPI credit card transactions as regular purchases with no fee, while others might add unexpected charges.

Who Should Actually Use This?

This makes sense for three types of people.

People who already use UPI daily and have a RuPay credit card. If you’re comfortable with UPI and want more payment flexibility, this is worth setting up.

People who need short-term cash flow help sometimes. Maybe payment is delayed or salary got held up. Using your credit limit via UPI bridges that gap without borrowing from friends or missing bill payments.

People who want credit card rewards on everyday purchases. If your card gives cashback or points, you can now earn on every tiny UPI payment. I get 1.2% cashback on my RuPay card, which adds up fast with ₹800 grocery runs three times weekly.

But if you struggle with credit card debt or overspend when money feels easy to access, skip this feature. It makes spending too frictionless, which can spiral quickly.

What I Wish Someone Had Told Me Earlier

You need stable internet when linking your card initially. I tried on sketchy cafe WiFi once the OTP timed out halfway. Use mobile data if WiFi is questionable.

Keep your credit card billing cycle in mind. I linked my card on the 18th, started using it for random purchases, then forgot my billing cycle ends on the 28th. Suddenly I had a bill due in 10 days I wasn’t prepared for.

Finally, treat this exactly like any other credit card payment. Just because it goes through UPI doesn’t make it different from swiping at a store. Same rules apply spend what you can pay back, don’t let interest pile up, and don’t confuse your credit limit with money you actually have.

I’ve been using this setup for about 7 weeks now. Feels normal. Just another way to pay for stuff, except now I have more options when my bank account looks sad.