Most people who start a SIP — a Systematic Investment Plan — do so with good intentions. They pick a fund, set up an auto-debit, and hope for the best. Then the market drops. Their portfolio goes red. They start second-guessing everything and, more often than not, they pause or stop the SIP entirely. That is usually the worst thing they could do.

The SIP 7-5-3-1 rule exists precisely to prevent that kind of panic-driven mistake. It is not a complicated mathematical formula. It is a four-part mental framework — a checklist of sorts — that tells you how long to invest, how to spread your money, how to handle your emotions, and how to grow your investment over time. Simple as that sounds, following it consistently is what separates investors who build real wealth from those who keep starting over.

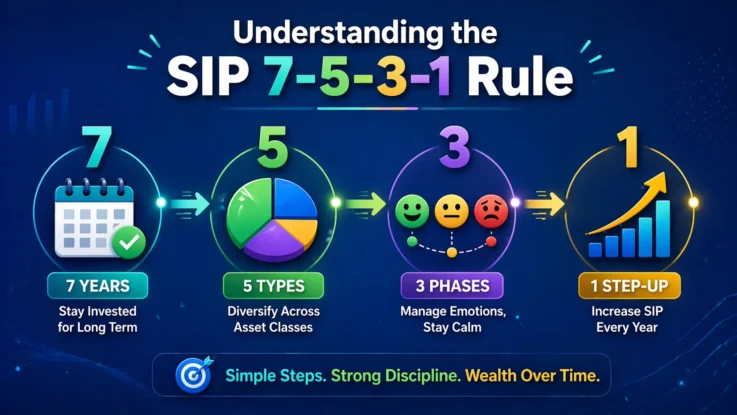

Let us go through each number, one at a time.

7 — Stay Invested for at Least 7 Years

The first number is about time, and it is probably the most important one of the four.

Equity mutual funds — the kind most SIP investors are in — are not designed for short-term goals. If you need money in two years to pay for a vacation or a gadget, a SIP in an equity fund is the wrong tool. But if your goal is seven or more years away — a child’s college education, a down payment on a home, or retirement — equity SIPs start to make a lot more sense.

Here is why seven years matters specifically. Over rolling seven-year periods, Indian equity markets have historically delivered better risk-adjusted returns than most other asset classes available to retail investors. Yes, there will be crashes along the way. There will be years when your portfolio is down 20 or 30 percent on paper. But the longer you stay invested, the more those dips get absorbed into the overall growth trajectory.

Compounding also needs time to do its job properly. In the early years of a SIP, the returns feel modest. You look at your statement and wonder if it is even worth it. But around year five or six, something shifts. The base gets large enough that even modest percentage gains start translating into meaningful rupee amounts. By year ten or fifteen, the numbers can look genuinely impressive — not because of some magic, but because compounding had enough time to build on itself.

The practical rule here is simple: do not start an equity SIP unless you are willing and able to leave it untouched for at least seven years. If your goal is shorter than that, consider debt funds or hybrid funds instead.

5 — Spread Your Money Across 5 Types of Funds

The second number is about diversification, and it addresses one of the most common mistakes new SIP investors make: putting all their money into one or two funds and then watching those funds underperform for a couple of years.

Also Read: Best Stocks to Buy This Month

The idea here is to spread your SIP contributions across roughly five different categories of funds or asset types. This does not mean five different mutual fund houses — it means five different styles or segments of the market, each of which tends to behave differently across market cycles.

A typical five-bucket setup might look something like this:

- Large-cap funds, which invest in well-established, blue-chip companies. These are the most stable of the equity categories and form the core of a sensible portfolio.

- Mid-cap funds, which invest in mid-sized companies that are growing faster than the large-caps but also carry more volatility. Higher risk, higher potential reward.

- Small-cap or flexi-cap funds, which go after smaller companies with high growth potential. These can be quite volatile in the short run but can deliver strong returns over long horizons.

- Value or focused funds, which follow a different investing philosophy — looking for undervalued companies rather than just the most popular ones. These can do well in certain market cycles when growth stocks are out of favour.

- International or hybrid funds, which add either global exposure or a mix of equity and debt, giving your portfolio a cushion during domestic market downturns.

You do not need to follow this exact mix. The specific allocation depends on your risk appetite, age, and goals. But the core principle holds: no single fund category dominates every market phase, so spreading across five gives your portfolio the resilience to weather different conditions.

Avoid the trap of owning five different schemes from the same category — say, five different large-cap funds. That is not diversification. That is concentration with extra paperwork. True diversification comes from owning funds that behave differently from each other.

3 — Prepare for 3 Emotional Phases of the Market

This is the part of the rule that most financial frameworks skip — the emotional side of investing. And yet it is arguably the most practically important.

When you invest in equity through a SIP over many years, you will go through at least three distinct emotional phases. Knowing what they are ahead of time does not make them disappear, but it does help you recognise them when they arrive, which makes it much easier to stay rational.

The first phase is disappointment. This usually shows up in the early years of a SIP, when your returns are either flat or lower than you expected. You look at your statement, compare it to a fixed deposit, and start wondering why you bothered. This phase is completely normal. Equity takes time to compound, and the early years are often the most frustrating. The right response is to do nothing — keep the SIP running.

The second phase is irritation. This happens when markets move sideways or fall moderately for an extended period. You are not losing sleep over it, but it is annoying. You might start reading about other funds that seem to be doing better, or wondering if you picked the wrong scheme. Again, the right response is to stay put. Switching funds mid-journey based on short-term performance comparisons is one of the most reliable ways to destroy long-term returns.

The third phase is panic. This is the big one — a sharp market crash, the kind that makes headlines and causes portfolios to drop 30 or 40 percent in a matter of weeks. Everything feels catastrophic. Your instinct screams at you to stop the SIP and pull your money out before it gets worse.

Here is the thing about panic phases: they are actually the best time to be running a SIP. When markets crash, every monthly instalment buys more units at lower prices. When the market eventually recovers — and historically, it always has — those cheap units generate outsized returns. Stopping your SIP at the bottom locks in your losses and means you miss the recovery entirely.

The 7-5-3-1 rule asks you to name these three phases before you start investing, so that when they arrive, you recognise them as normal parts of the journey rather than signs that something has gone terribly wrong.

1 — Increase Your SIP Amount Once Every Year

The fourth number is about growth — specifically, growing your SIP in line with your growing income.

Most people set up a SIP at, say, ₹5,000 or ₹10,000 per month and then leave it at that amount for years, even as their salary increases. The logic feels sound: you are already investing, so why change anything? But this approach has a quiet cost. As inflation rises and your income grows, that fixed ₹10,000 represents a smaller and smaller percentage of what you earn. In real terms, you are investing less and less over time.

The rule suggests increasing your SIP amount once a year — typically by around 10 percent, roughly in line with salary growth or a little more. This is sometimes called a step-up SIP, and many investment platforms now offer it as an automatic feature.

The mathematics here is surprisingly powerful. If you start with a ₹10,000 monthly SIP and increase it by 10 percent each year, the final corpus after 15 years can be nearly double what you would have accumulated with a flat ₹10,000 SIP throughout — even if the fund returns are identical in both cases. You are not timing the market or taking extra risk. You are simply putting more money to work, compounding on a larger base, every year.

The practical way to do this is to tie your annual SIP review to something you already do — like filing your taxes or getting your salary hike. When you get a raise in April, increase your SIP in May. Make it a habit rather than a decision you have to actively make each time.

Quick Reference: The 7-5-3-1 Rule at a Glance

| Number | What It Means | Why It Matters | What To Do |

| 7 | Invest for at least 7 years | Equity compounds best over long horizons | Don’t exit equity before 7 years |

| 5 | Diversify across ~5 fund types | Reduces concentration risk | Spread across large, mid, small, value, hybrid/international |

| 3 | Prepare for 3 emotional phases | Prevents panic selling at the worst time | Recognise disappointment, irritation, panic — and stay invested |

| 1 | Step up your SIP once a year (~10%) | Grows corpus significantly without extra risk | Increase SIP every year in line with income growth |

What This Rule Cannot Do

It is worth being honest about what the 7-5-3-1 rule is and is not. It is a behavioural guide — a set of guardrails for long-term investors. It is not a return calculator, and it does not guarantee specific outcomes. Markets can underperform for extended periods. Fund managers can make poor decisions. Macroeconomic conditions can shift in ways that nobody predicted.

The rule also works best for medium-to-long-term equity goals. It is not designed for the money you might need in the next year or two. If your goal is short-term, this framework does not apply.

And crucially, “five funds” is a guideline, not a magic number. Some investors do perfectly well with three. Others might have a case for six or seven. The underlying principle — spread your money across different market segments — matters more than hitting an exact count.

Also Read: Bonds vs Stocks: Key Differences Between Two of the Most Crucial Investment Options

Is the 7-5-3-1 Rule Worth Following?

For most retail investors in India who are investing through SIPs for long-term goals, yes — absolutely. Not because it is a sophisticated strategy, but because it addresses the four things that tend to derail ordinary investors: stopping too soon, concentrating too heavily, reacting emotionally, and failing to grow contributions over time.

The best investing strategy is the one you can actually stick to. The 7-5-3-1 rule is easy enough to remember, broad enough to apply to most situations, and grounded in enough real-world logic that following it faithfully will serve the vast majority of long-term SIP investors well.

Start long. Spread wide. Stay calm. Step up. Four principles, four numbers, one consistent habit. That is really all it takes.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Please consult a SEBI-registered financial advisor before making investment decisions.