Let me ask you something. If someone handed you ₹1 lakh right now and told you to invest it, what would you do?

Most people freeze at that question. Not because they don’t want to invest, but because the moment they start researching, two words keep showing up everywhere: bonds and stocks. And somewhere between reading contradictory advice on the internet and watching their neighbour brag about equity returns at a dinner party, they end up doing nothing.

This paralysis often stems from a lack of understanding of what these two instruments are, how they differ, and which one is appropriate for a specific situation. So let’s fix that. No jargon. No lecture. Just a clear, honest breakdown of bonds vs stocks so you can make decisions with confidence.

What Are Stocks?

Think of a stock as a tiny slice of a company. When a business wants to raise money—to expand, launch new products, or pay off debt—it can sell its pieces to the public. Those pieces are shares or stocks. When you buy a share of a company, you become a part-owner of that business. Small part, sure. But a genuine owner.

As a shareholder, you stand to benefit in two main ways. First, if the company grows and its stock price rises, the value of your investment goes up — this increase is called capital appreciation. Second, some companies distribute a portion of their profits to shareholders in the form of dividends.

The catch? Neither of these is guaranteed. Stock prices go up, and they go down — sometimes dramatically — based on company performance, market sentiment, economic conditions, and a dozen other factors. This is why stocks are considered a higher-risk investment. The potential upside is significant. So is the potential downside.

What Are Bonds?

Bonds work very differently. When you buy a bond, you’re not buying ownership of anything. You’re lending money — to a government, a corporation, or a municipal body — for a fixed period of time. In return, they promise to pay you regular interest (called the coupon rate) and return your original principal when the bond matures.

It’s a straightforward transaction. You lend ₹1 lakh. They pay you, say, 7% interest every year for five years. At the end of five years, you get your ₹1 lakh back. The terms are agreed upon up front. There’s no guessing, no waiting to see if a quarterly earnings report beats expectations.

This predictability is what makes bonds attractive, particularly for conservative investors, retirees, or anyone who needs their money to be working steadily in the background without dramatic swings.

Bonds vs Stocks: The Core Differences

Also Read: Best Stocks to Buy This Month

Let’s put this side by side clearly.

Nature of the investment: Stocks are equity — you own a piece of the company. Bonds are debt — you’ve lent money to an issuer who owes it back to you with interest.

Returns: Stock returns come from price appreciation and dividends—both are variable and neither is guaranteed. Bond returns come from fixed interest payments — predictable, scheduled, and agreed upon upfront.

Risk: Stocks carry a higher risk. Prices fluctuate based on market forces, and in a bad scenario, a company’s stock can lose significant value. Bonds are generally safer, especially government bonds, though they’re not entirely risk-free. If an issuer defaults, bondholders can lose money, too.

Who issues them: Stocks are issued only by corporations. Bonds can be issued by national governments, state and city governments, corporations, and even supranational institutions.

In liquidation: If a company winds up, bondholders get paid before shareholders. This is a critical distinction — as a bondholder, you have legal priority. As a stockholder, you’re last in line.

Taxation: Stock returns — particularly dividends — may attract dividend distribution tax depending on the structure. Bond interest income is taxable as regular income, though certain government bonds come with tax exemptions.

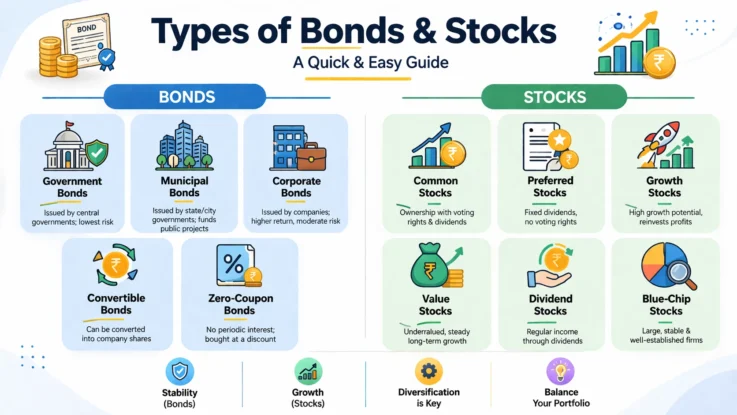

Types of Bonds

Not all bonds are the same. Here are the main categories:

Government bonds — issued by the central government, considered the safest since they’re backed by a sovereign guarantee. In India, these include G-secs and treasury bills.

Municipal bonds — issued by state or city governments to fund public infrastructure like roads, schools, or water systems.

Corporate bonds — issued by companies seeking to raise debt capital. Higher yields than government bonds, but with greater credit risk.

Convertible bonds — these start as bonds but can be converted into equity shares under certain conditions. Often used by high-growth companies.

Zero-coupon bonds — these don’t pay regular interest. Instead, they’re issued at a discount and redeemed at face value — the difference being your return.

Types of Stocks

Stocks come in more varieties than most people realize:

Common stock — the standard form, offering voting rights and potential dividends. Most individual investors hold common stock.

Preferred stock — offers fixed dividends and priority over common stockholders in liquidation but typically has no voting rights.

Growth stock — companies that reinvest profits for expansion rather than paying dividends. Higher risk, higher potential reward.

Value stock — trading below what analysts consider the company’s true worth. The classic “buy low” opportunity.

Dividend or income stock — companies known for regular, reliable dividend payments. Popular among investors who want passive income.

Blue-chip stock — large, established, financially sound companies with a long track record. Think of the Nifty 50 heavyweights. Lower excitement, higher reliability.

Penny stock — low-priced stocks with small market capitalization. High risk, often highly speculative.

Risk and Returns: The Honest Comparison

Here’s the thing that gets glossed over in most financial content — it’s not that one is better than the other. It’s that they serve different purposes.

If you’re 28 years old with a steady income, a long investment horizon, and the stomach to watch your portfolio dip 20% in a bad quarter without panicking, stocks offer the kind of long-term wealth-building potential that bonds simply can’t match.

If you’re 58, approaching retirement, with financial obligations that require a steady income and limited capacity to absorb losses, bonds offer the stability and predictability that stocks won’t.

Most smart investors don’t choose between bonds and stocks. They hold both in a ratio that reflects their age, goals, income, and risk tolerance. This is what proper portfolio diversification looks like — not picking a winner, but building a balance.

A common rule of thumb in personal finance circles is to subtract your age from 100 — that’s roughly the percentage of your portfolio to hold in equities. The rest goes into debt instruments like bonds. It’s not a perfect formula, but it’s a starting point worth considering.

Also Read: Best Health Insurance Companies in India 2026 – Honest Guide

So, Which One Should You Choose?

The honest answer is probably both, in the right proportion.

If growth and long-term wealth creation are the priority, lean toward stocks. Accept the volatility as the price of higher returns. Stay invested through market cycles and resist the urge to sell every time markets drop.

If capital preservation and predictable income matter more, bonds deserve a meaningful allocation in your portfolio. They won’t make you rich quickly, but they’ll keep your money safe and working steadily.

The investors who make the most consistent long-term gains aren’t the ones who pick one over the other. They’re the ones who understand them both deeply enough to use each one exactly where it belongs.

That understanding starts right here. The rest is just execution.

Quick Reference: Bonds vs Stocks at a Glance

| Parameter | Bonds | Stocks |

|---|---|---|

| Type | Debt instrument | Equity instrument |

| Issuer | Government, corporates, municipalities | Corporations |

| Returns | Fixed interest (coupon) | Dividends + capital appreciation |

| Risk level | Lower | Higher |

| Investor benefit | Priority in repayment | Voting rights + ownership |

| Market | OTC / bond market | Stock exchanges |

| Taxation | Interest taxable as income | A dividend tax may apply |

| Best suited for | Conservative / income investors | Growth-oriented investors |